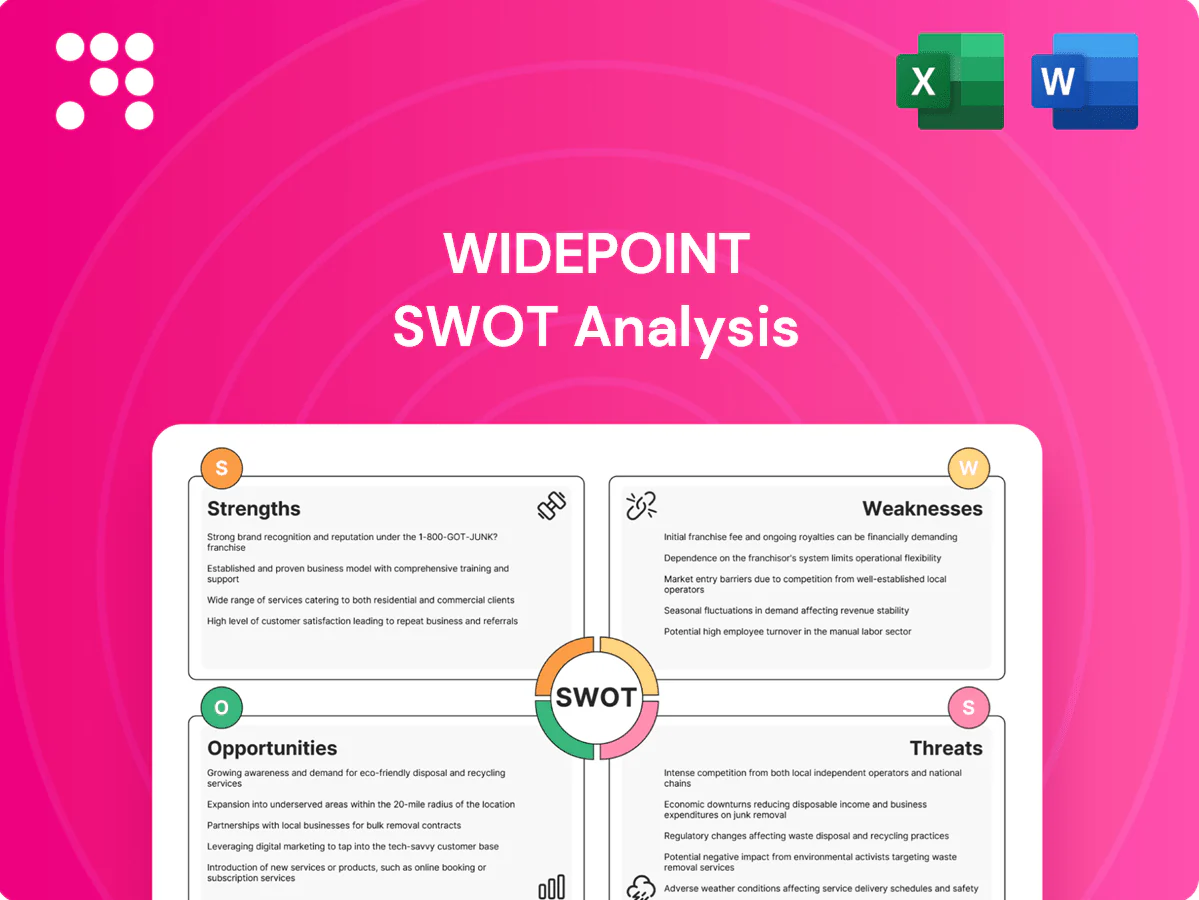

Carl Zeiss Meditec SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

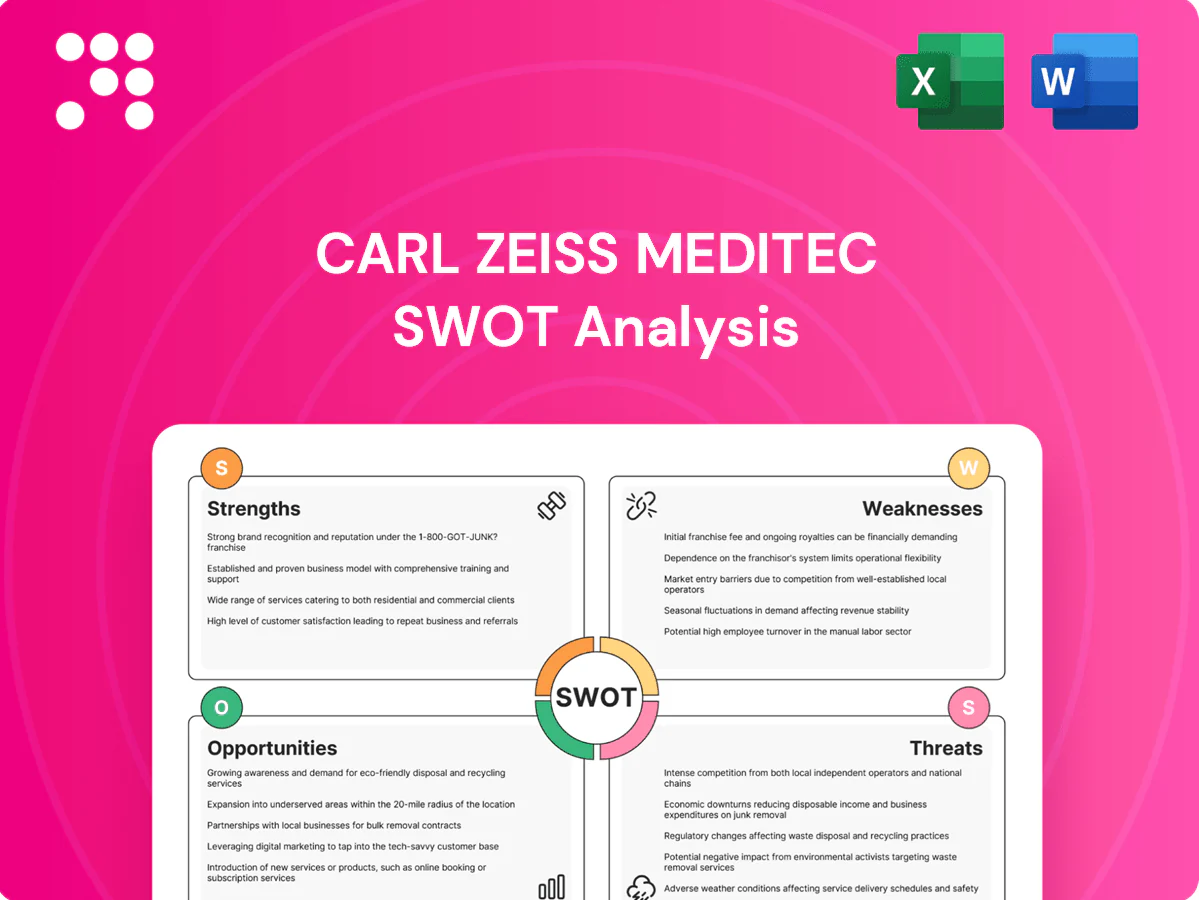

Carl Zeiss Meditec combines premium optics and strong surgical device R&D, giving it a competitive edge in ophthalmic markets. Regulatory exposure, pricing pressure, and supply-chain risks could challenge near-term margins. Growth opportunities include an aging population and emerging markets expansion. Purchase the full SWOT analysis for a detailed, editable report to guide investment or strategy decisions.

Strengths

Premium ZEISS brand trust

The ZEISS name conveys precision, reliability and clinical credibility in ophthalmology and microsurgery, underpinning Carl Zeiss Meditec’s reported €1.6bn revenue in FY 2024 and presence in 100+ countries. This brand equity helps win hospital tenders and access premium private markets, supporting persistent pricing power. It reduces adoption friction for new platforms and strong KOL relationships amplify perceived quality and reported clinical outcomes.

Comprehensive end‑to‑end portfolio

Carl Zeiss Meditec delivers a comprehensive end‑to‑end portfolio covering diagnostics, planning, therapy, surgical microscopes and intraocular lenses in one integrated workflow, supporting seamless patient pathways. Integrated solutions improve clinical outcomes and operational efficiency, helping clinics reduce turnaround and increase throughput; ZEISS Meditec reported c.€1.8bn revenue in FY 2024, reflecting strong demand. Cross‑selling across the care pathway raises customer lifetime value, while one‑vendor simplicity boosts stickiness and service attach rates.

Deep optical and engineering know‑how

Core competencies in optics, imaging and mechatronics give Carl Zeiss Meditec superior visualization and procedural accuracy; FY 2023/24 revenue of about €1.73bn underpins scale advantages. Continuous R&D (≈€150m, ~8.7% of sales) produces incremental and step‑change advances. Proprietary algorithms and software boost device performance, creating a technical moat hard for rivals to replicate quickly.

Large installed base with recurring revenue

Large global installed base drives recurring revenue through service contracts, software subscriptions and consumables, delivering high uptime and lifecycle services that produce predictable cash flows; platform upgrades extend device relevance and margin capture, while data feedback loops from deployed systems accelerate product improvements.

- Recurring service, software, consumables

- High uptime → predictable cash flows

- Upgrades boost margins

- Installed-data informs R&D

Global distribution and clinical partnerships

Carl Zeiss Meditec leverages direct and indirect channels across key regions and segments to ensure broad market reach, while clinical partnerships with leading surgeons and institutions accelerate evidence generation and technology adoption. Established training ecosystems increase utilization and improve outcomes, and robust post‑sale support drives retention and referral growth.

- Global channel coverage

- Surgeon & institutional ties

- Training ecosystems

- Strong post‑sale support

Ophthalmology leader: ≈€1.7bn, R&D ≈€150m (≈8.7%)

ZEISS brand drives clinical trust and pricing power, supporting ≈€1.7bn revenue in FY2024 and presence in 100+ countries.

End‑to‑end ophthalmology portfolio boosts cross‑sell, workflow stickiness and higher customer lifetime value.

R&D ≈€150m (~8.7% of sales) and proprietary optics/software create a technical moat.

Large installed base yields recurring service, software and consumables revenue with predictable cash flows.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈€1.7bn |

| R&D spend | ≈€150m (≈8.7%) |

| Geographic reach | 100+ countries |

What is included in the product

Provides a concise SWOT analysis of Carl Zeiss Meditec, highlighting its technological strengths and market positioning, key operational weaknesses, growth opportunities in ophthalmic and surgical markets, and external threats from competition and regulatory pressures.

Provides a concise SWOT matrix for Carl Zeiss Meditec to quickly surface strategic risks and opportunities, easing executive decision-making and aligning strategy across clinical, R&D, and market teams.

Weaknesses

High price points and capital intensity

Premium Carl Zeiss Meditec devices demand substantial upfront investment from providers, with advanced surgical systems and imaging platforms commonly costing into the low- to mid-six-figure range, which constrains purchases. Budget limits and public tender dynamics slow conversions, particularly in hospitals facing capital rationing. Demonstrating ROI often requires multi-year clinical and throughput data, extending sales cycles beyond a year. Price sensitivity in emerging markets limits penetration against lower-cost competitors.

Concentration in ophthalmology

Revenue remains concentrated in ophthalmology, accounting for over 70% of Carl Zeiss Meditec sales, so product or reimbursement shifts in eye care (US, EU) can materially affect top-line performance.

Segment shocks or policy changes—e.g., reimbursements for cataract or retinal procedures—have historically driven quarter-to-quarter volatility in volumes and margins.

Diversification into adjacent therapies is modest versus large diversified med‑tech peers, increasing downside sensitivity in industry downcycles.

Lower scale versus mega‑competitors

Lower scale versus mega‑competitors leaves Carl Zeiss Meditec vulnerable as larger rivals outspend it on marketing and R&D, enabling broader portfolio bundling to win hospital tenders; scale disadvantages can compress gross margins and force price concessions, while competing for niche ophthalmic and surgical talent is harder when peers offer bigger R&D programs and broader career paths.

Complexity of integrated workflows

Complex integrated workflows raise implementation risk for Carl Zeiss Meditec as interoperability and data integration can delay deployments and erode ROI; FY2024 revenue was about 1.8 billion EUR, so ramp delays impact material top-line timing. Extensive training requirements slow utilization and time-to-value, while custom site configurations increase ongoing service burden and costs. Any persistent integration gaps can negate promised efficiency gains and pressure service margins.

- Interoperability risk

- Training slows utilization

- Customization raises service load

- Integration gaps cut efficiency

Exposure to European market dynamics

Significant European activity—≈50% of group sales in 2024—raises MDR compliance burden and recurring certification costs, squeezing margins and CAPEX for regulatory upgrades. Macro softness and intensified public tenders in key markets have pressured pricing, while 2024 currency moves (EUR vs USD ~8% swing) added noticeable earnings variability. Shifts in regional procurement policies can rapidly alter hospital buying patterns and replacement cycles.

- Exposure: ≈50% sales in Europe (2024)

- Regulatory: higher MDR compliance costs

- Pricing: tender-driven margin pressure

- FX: ~8% EUR/USD swing in 2024

Premium devices: FY2024 revenue ~1.8bn EUR; >70% ophthalmology; ≈50% Europe

Premium devices demand high upfront spend (FY2024 revenue ~1.8bn EUR). Over 70% of sales are ophthalmology, concentrating revenue risk. ≈50% of sales in Europe raises MDR/regulatory costs and tender pressure; EUR/USD swung ~8% in 2024, adding earnings volatility.

| Metric | Value |

|---|---|

| FY2024 revenue | ~1.8bn EUR |

| Ophthalmology share | >70% |

| Europe share | ≈50% |

| EUR/USD 2024 swing | ~8% |

Full Version Awaits

Carl Zeiss Meditec SWOT Analysis

This is the actual Carl Zeiss Meditec SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering strengths, weaknesses, opportunities and threats. This is a real excerpt from the complete, editable file and the full content is unlocked after payment.

Original: $10.00

-70%$10.00

$3.00

Description

Go Beyond the Preview—Access the Full Strategic Report

Carl Zeiss Meditec combines premium optics and strong surgical device R&D, giving it a competitive edge in ophthalmic markets. Regulatory exposure, pricing pressure, and supply-chain risks could challenge near-term margins. Growth opportunities include an aging population and emerging markets expansion. Purchase the full SWOT analysis for a detailed, editable report to guide investment or strategy decisions.

Strengths

Premium ZEISS brand trust

The ZEISS name conveys precision, reliability and clinical credibility in ophthalmology and microsurgery, underpinning Carl Zeiss Meditec’s reported €1.6bn revenue in FY 2024 and presence in 100+ countries. This brand equity helps win hospital tenders and access premium private markets, supporting persistent pricing power. It reduces adoption friction for new platforms and strong KOL relationships amplify perceived quality and reported clinical outcomes.

Comprehensive end‑to‑end portfolio

Carl Zeiss Meditec delivers a comprehensive end‑to‑end portfolio covering diagnostics, planning, therapy, surgical microscopes and intraocular lenses in one integrated workflow, supporting seamless patient pathways. Integrated solutions improve clinical outcomes and operational efficiency, helping clinics reduce turnaround and increase throughput; ZEISS Meditec reported c.€1.8bn revenue in FY 2024, reflecting strong demand. Cross‑selling across the care pathway raises customer lifetime value, while one‑vendor simplicity boosts stickiness and service attach rates.

Deep optical and engineering know‑how

Core competencies in optics, imaging and mechatronics give Carl Zeiss Meditec superior visualization and procedural accuracy; FY 2023/24 revenue of about €1.73bn underpins scale advantages. Continuous R&D (≈€150m, ~8.7% of sales) produces incremental and step‑change advances. Proprietary algorithms and software boost device performance, creating a technical moat hard for rivals to replicate quickly.

Large installed base with recurring revenue

Large global installed base drives recurring revenue through service contracts, software subscriptions and consumables, delivering high uptime and lifecycle services that produce predictable cash flows; platform upgrades extend device relevance and margin capture, while data feedback loops from deployed systems accelerate product improvements.

- Recurring service, software, consumables

- High uptime → predictable cash flows

- Upgrades boost margins

- Installed-data informs R&D

Global distribution and clinical partnerships

Carl Zeiss Meditec leverages direct and indirect channels across key regions and segments to ensure broad market reach, while clinical partnerships with leading surgeons and institutions accelerate evidence generation and technology adoption. Established training ecosystems increase utilization and improve outcomes, and robust post‑sale support drives retention and referral growth.

- Global channel coverage

- Surgeon & institutional ties

- Training ecosystems

- Strong post‑sale support

Ophthalmology leader: ≈€1.7bn, R&D ≈€150m (≈8.7%)

ZEISS brand drives clinical trust and pricing power, supporting ≈€1.7bn revenue in FY2024 and presence in 100+ countries.

End‑to‑end ophthalmology portfolio boosts cross‑sell, workflow stickiness and higher customer lifetime value.

R&D ≈€150m (~8.7% of sales) and proprietary optics/software create a technical moat.

Large installed base yields recurring service, software and consumables revenue with predictable cash flows.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈€1.7bn |

| R&D spend | ≈€150m (≈8.7%) |

| Geographic reach | 100+ countries |

What is included in the product

Provides a concise SWOT analysis of Carl Zeiss Meditec, highlighting its technological strengths and market positioning, key operational weaknesses, growth opportunities in ophthalmic and surgical markets, and external threats from competition and regulatory pressures.

Provides a concise SWOT matrix for Carl Zeiss Meditec to quickly surface strategic risks and opportunities, easing executive decision-making and aligning strategy across clinical, R&D, and market teams.

Weaknesses

High price points and capital intensity

Premium Carl Zeiss Meditec devices demand substantial upfront investment from providers, with advanced surgical systems and imaging platforms commonly costing into the low- to mid-six-figure range, which constrains purchases. Budget limits and public tender dynamics slow conversions, particularly in hospitals facing capital rationing. Demonstrating ROI often requires multi-year clinical and throughput data, extending sales cycles beyond a year. Price sensitivity in emerging markets limits penetration against lower-cost competitors.

Concentration in ophthalmology

Revenue remains concentrated in ophthalmology, accounting for over 70% of Carl Zeiss Meditec sales, so product or reimbursement shifts in eye care (US, EU) can materially affect top-line performance.

Segment shocks or policy changes—e.g., reimbursements for cataract or retinal procedures—have historically driven quarter-to-quarter volatility in volumes and margins.

Diversification into adjacent therapies is modest versus large diversified med‑tech peers, increasing downside sensitivity in industry downcycles.

Lower scale versus mega‑competitors

Lower scale versus mega‑competitors leaves Carl Zeiss Meditec vulnerable as larger rivals outspend it on marketing and R&D, enabling broader portfolio bundling to win hospital tenders; scale disadvantages can compress gross margins and force price concessions, while competing for niche ophthalmic and surgical talent is harder when peers offer bigger R&D programs and broader career paths.

Complexity of integrated workflows

Complex integrated workflows raise implementation risk for Carl Zeiss Meditec as interoperability and data integration can delay deployments and erode ROI; FY2024 revenue was about 1.8 billion EUR, so ramp delays impact material top-line timing. Extensive training requirements slow utilization and time-to-value, while custom site configurations increase ongoing service burden and costs. Any persistent integration gaps can negate promised efficiency gains and pressure service margins.

- Interoperability risk

- Training slows utilization

- Customization raises service load

- Integration gaps cut efficiency

Exposure to European market dynamics

Significant European activity—≈50% of group sales in 2024—raises MDR compliance burden and recurring certification costs, squeezing margins and CAPEX for regulatory upgrades. Macro softness and intensified public tenders in key markets have pressured pricing, while 2024 currency moves (EUR vs USD ~8% swing) added noticeable earnings variability. Shifts in regional procurement policies can rapidly alter hospital buying patterns and replacement cycles.

- Exposure: ≈50% sales in Europe (2024)

- Regulatory: higher MDR compliance costs

- Pricing: tender-driven margin pressure

- FX: ~8% EUR/USD swing in 2024

Premium devices: FY2024 revenue ~1.8bn EUR; >70% ophthalmology; ≈50% Europe

Premium devices demand high upfront spend (FY2024 revenue ~1.8bn EUR). Over 70% of sales are ophthalmology, concentrating revenue risk. ≈50% of sales in Europe raises MDR/regulatory costs and tender pressure; EUR/USD swung ~8% in 2024, adding earnings volatility.

| Metric | Value |

|---|---|

| FY2024 revenue | ~1.8bn EUR |

| Ophthalmology share | >70% |

| Europe share | ≈50% |

| EUR/USD 2024 swing | ~8% |

Full Version Awaits

Carl Zeiss Meditec SWOT Analysis

This is the actual Carl Zeiss Meditec SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering strengths, weaknesses, opportunities and threats. This is a real excerpt from the complete, editable file and the full content is unlocked after payment.