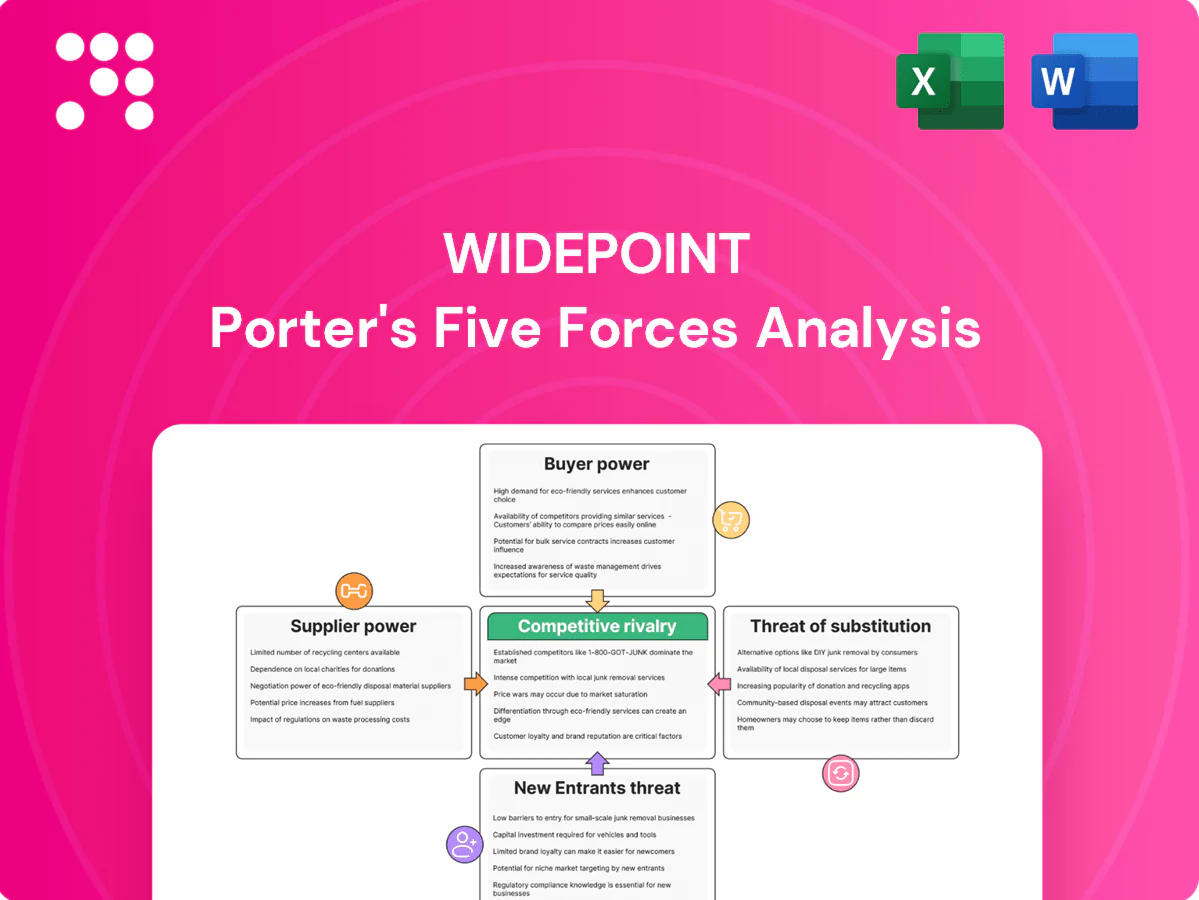

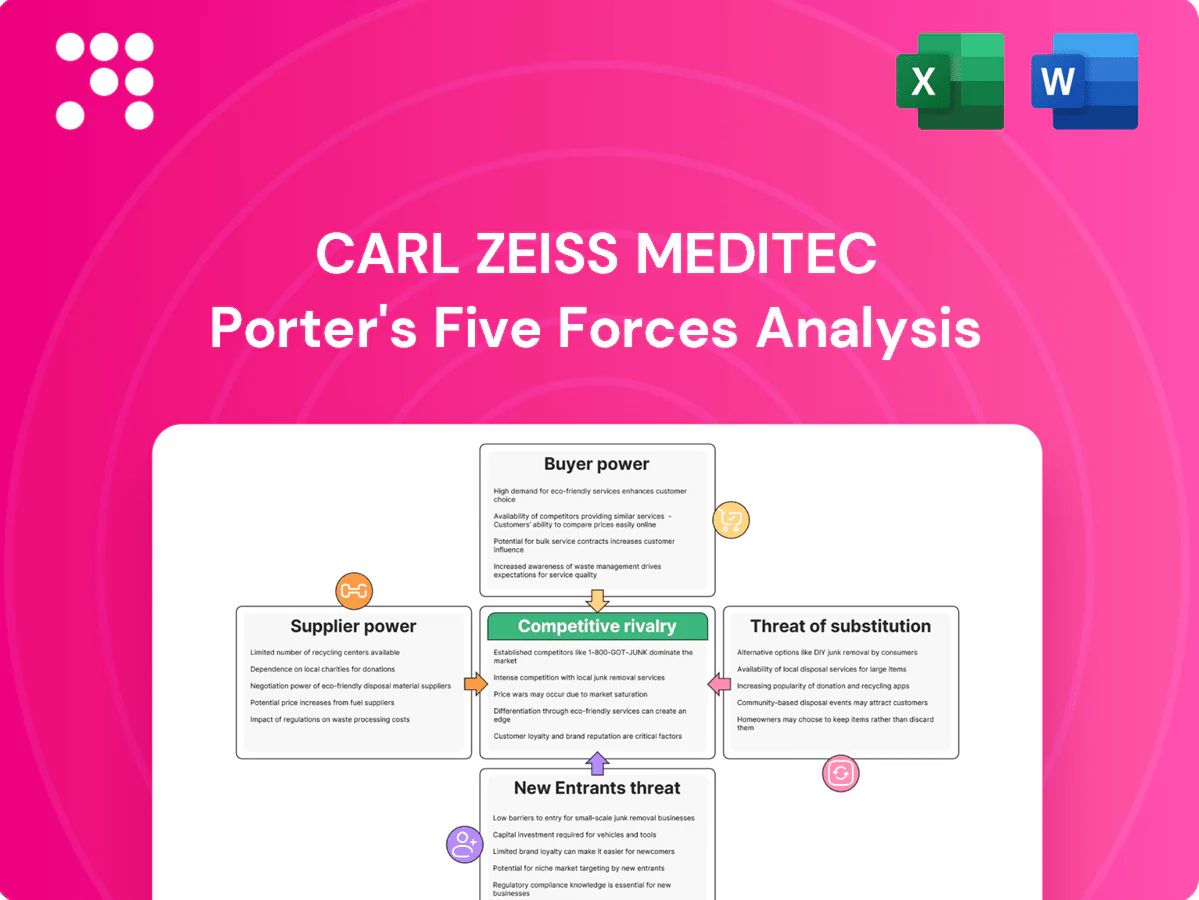

Carl Zeiss Meditec Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Carl Zeiss Meditec faces moderate buyer power, specialized suppliers, and strong rivalry driven by innovation. High entry barriers limit newcomers, but niche substitutes and price pressure exist. Regulatory risk affects margins and strategy. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Carl Zeiss Meditec.

Suppliers Bargaining Power

Precision optics and sensors

High-spec glass, coatings and image sensors for Carl Zeiss Meditec come from a limited pool of qualified vendors, concentrating bargaining power with niche suppliers. Tight tolerances and regulatory-grade traceability further reduce switching options, pressuring margins for a company with 2024 revenue around EUR 1.9bn. This supplier concentration elevates supply risk, which long-term contracts and dual-sourcing can partially mitigate in a global image sensor market near $22bn in 2024.

Software and algorithm components

AI/diagnostics modules and embedded software rely on specialized toolchains and third-party libraries, and certification/revalidation is costly—often exceeding six figures—creating strong lock-in for vendors. Suppliers of critical software IP can therefore command favorable terms and margins. Carl Zeiss Meditec faces this amid a market with over 600 FDA-cleared AI medical devices by 2024, so in-house development offsets supplier risk but raises fixed R&D costs significantly.

Mechatronics and robotics subsystems

Precision stages, lasers and actuators for medical devices are supplied by fewer than 10 medical-grade providers, and 2024 lead times have commonly exceeded 20 weeks for customized subsystems, increasing dependency and exposure. High customization forces OEMs like Carl Zeiss Meditec to offer volume commitments or pay premiums to secure capacity. These dynamics strengthen supplier leverage over price and on-time delivery, raising procurement and inventory costs.

Sterile consumables and IOL materials

Sterile consumables and IOL materials require ISO 13485 and ISO 10993 biocompatibility compliance, with qualification and sterilization validation often taking 3–12 months, deterring rapid supplier changes and raising effective switching costs for Carl Zeiss Meditec. Approved supplier lists and regulatory audits narrow sourcing flexibility, concentrating bargaining power with certified polymer and sterilization providers.

- Long validation timelines: 3–12 months

- Standards: ISO 13485, ISO 10993

- High switching cost: regulatory & audit overhead

Geopolitical and supply chain concentration

Geopolitical and supply‑chain concentration raises supplier bargaining power for Carl Zeiss Meditec: in 2024 East Asia (notably Taiwan and South Korea) accounted for roughly 60–65% of global advanced semiconductor and optics component capacity, heightening disruption risk from regional shocks and export controls.

US and allied export controls on advanced chips and ASML EUV restrictions in 2023–24 increased supplier leverage through licensing and quality audits, forcing customers into longer lead times or stricter compliance.

Buffer inventories and nearshoring reduce outage risk but pushed working capital higher in 2024, so net supplier power is moderate-to-high for ZEISS Meditec.

- 2024: East Asia ~60–65% of advanced component capacity

- 2023–24: export controls and EUV limits amplified supplier influence

- Mitigants: buffer stock and nearshoring raise working capital

- Net: moderate-to-high supplier power

Moderate-high supplier power; 3-12m validation and 60-65% East Asia reliance

Supplier power is moderate–high for Carl Zeiss Meditec: limited optics/sensor vendors and long validation (3–12 months) squeeze margins despite 2024 revenue ~EUR1.9bn. East Asia supplied ~60–65% of advanced components in 2024; image-sensor market ~$22bn. Dual-sourcing and buffers mitigate risk but raise working capital.

| Metric | 2024 |

|---|---|

| Revenue | EUR 1.9bn |

| East Asia share | 60–65% |

| Image-sensor mkt | $22bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Carl Zeiss Meditec, with detailed assessment of threats from substitutes and new entrants. Evaluates supplier and buyer power, identifies disruptive forces, and highlights strategic levers that protect incumbency and drive sustainable profitability.

Clear, one-sheet Porter's Five Forces for Carl Zeiss Meditec—instantly visualize competitive pressure with a radar chart, customize inputs for regulatory shifts or new entrants, and drop the clean layout straight into pitch decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Large hospital systems and GPOs

Large hospital systems and GPOs exert strong buyer power: group purchasing and tenders drive price pressure and standardization, with GPOs accounting for around 70% of US hospital purchasing in 2024, enabling buyers to extract volume discounts and bundled service deals. Multi-year framework agreements shift leverage to sophisticated purchasers, forcing vendors like Carl Zeiss Meditec to compete on total cost of ownership, not just unit price.

Ophthalmology chains and ASCs

High throughput in ophthalmology—about 3.7 million US cataract procedures annually and ~20 million globally in 2024—makes device uptime and per-procedure cost critical for chains and ASCs. Buyers run detailed ROI models comparing platforms, and brand switching at expansion points raises their bargaining power. Service SLAs and financing terms routinely decide deals, often outweighing small tech differentials.

Reimbursement-driven decision making

Reimbursement-driven buying gives customers leverage: capital spend hinges on coding, coverage and tariff levels, so flat reimbursement prompts buyers to demand lower equipment prices or consumable discounts. Carl Zeiss Meditec reported revenue of EUR 1.74bn in FY2024, yet premium pricing depends on demonstrated clinical efficacy; evidence gaps weaken vendor pricing power. In the US Medicare covers about 80% of cataract procedures, amplifying payer influence.

Training and workflow integration

Deep EMR/PACS integration and surgeon training create high switching costs that reduce buyer power; as of 2024 over 96% of US hospitals use certified EHRs (ONC trend), increasing lock‑in for integrated devices, while interoperable offerings expand buyer options and post‑sale support quality materially shifts negotiation leverage.

- Integration lock‑in: high switching costs

- Interoperability: increases buyer options

- Support quality: major negotiation factor

International tender dynamics

Public international tenders for medical devices focus on lowest compliant bid and lifecycle cost, reinforcing price competition; OECD estimates public procurement at about 12% of GDP, underscoring scale and buyer leverage. Transparent, rule-based scoring in many jurisdictions limits differentiation premiums, while local content rules (increasingly used in 2020s) shift bargaining power to regional buyers; overall buyer power is moderate-to-high.

- OECD: public procurement ≈12% of GDP

- Lowest compliant bid + lifecycle costing → price-focused awards

- Transparent scoring reduces differentiation premiums

- Local content rules increase regional buyer leverage

- Buyer power: moderate-to-high

GPO-driven pricing and per-procedure cost dominate high-volume cataract device markets

Large hospital systems and GPOs (≈70% of US hospital purchasing in 2024) drive price pressure; buyers demand TCO, SLAs and bundled deals. High procedure volumes (~3.7M US cataracts, ~20M global in 2024) make per‑procedure cost and uptime decisive. Reimbursement dependence (Medicare ≈80% of US cataracts) increases buyer leverage; integration lock‑in partially offsets power.

| Metric | Value |

|---|---|

| GPO share (US) | ≈70% |

| Cataracts (US/global, 2024) | 3.7M / 20M |

| Meditec revenue FY2024 | EUR 1.74bn |

| Public procurement (OECD) | ≈12% GDP |

Preview the Actual Deliverable

Carl Zeiss Meditec Porter's Five Forces Analysis

This preview shows the exact Carl Zeiss Meditec Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the fully formatted, professional file ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical report.

Original: $10.00

-70%$10.00

$3.00

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Carl Zeiss Meditec faces moderate buyer power, specialized suppliers, and strong rivalry driven by innovation. High entry barriers limit newcomers, but niche substitutes and price pressure exist. Regulatory risk affects margins and strategy. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Carl Zeiss Meditec.

Suppliers Bargaining Power

Precision optics and sensors

High-spec glass, coatings and image sensors for Carl Zeiss Meditec come from a limited pool of qualified vendors, concentrating bargaining power with niche suppliers. Tight tolerances and regulatory-grade traceability further reduce switching options, pressuring margins for a company with 2024 revenue around EUR 1.9bn. This supplier concentration elevates supply risk, which long-term contracts and dual-sourcing can partially mitigate in a global image sensor market near $22bn in 2024.

Software and algorithm components

AI/diagnostics modules and embedded software rely on specialized toolchains and third-party libraries, and certification/revalidation is costly—often exceeding six figures—creating strong lock-in for vendors. Suppliers of critical software IP can therefore command favorable terms and margins. Carl Zeiss Meditec faces this amid a market with over 600 FDA-cleared AI medical devices by 2024, so in-house development offsets supplier risk but raises fixed R&D costs significantly.

Mechatronics and robotics subsystems

Precision stages, lasers and actuators for medical devices are supplied by fewer than 10 medical-grade providers, and 2024 lead times have commonly exceeded 20 weeks for customized subsystems, increasing dependency and exposure. High customization forces OEMs like Carl Zeiss Meditec to offer volume commitments or pay premiums to secure capacity. These dynamics strengthen supplier leverage over price and on-time delivery, raising procurement and inventory costs.

Sterile consumables and IOL materials

Sterile consumables and IOL materials require ISO 13485 and ISO 10993 biocompatibility compliance, with qualification and sterilization validation often taking 3–12 months, deterring rapid supplier changes and raising effective switching costs for Carl Zeiss Meditec. Approved supplier lists and regulatory audits narrow sourcing flexibility, concentrating bargaining power with certified polymer and sterilization providers.

- Long validation timelines: 3–12 months

- Standards: ISO 13485, ISO 10993

- High switching cost: regulatory & audit overhead

Geopolitical and supply chain concentration

Geopolitical and supply‑chain concentration raises supplier bargaining power for Carl Zeiss Meditec: in 2024 East Asia (notably Taiwan and South Korea) accounted for roughly 60–65% of global advanced semiconductor and optics component capacity, heightening disruption risk from regional shocks and export controls.

US and allied export controls on advanced chips and ASML EUV restrictions in 2023–24 increased supplier leverage through licensing and quality audits, forcing customers into longer lead times or stricter compliance.

Buffer inventories and nearshoring reduce outage risk but pushed working capital higher in 2024, so net supplier power is moderate-to-high for ZEISS Meditec.

- 2024: East Asia ~60–65% of advanced component capacity

- 2023–24: export controls and EUV limits amplified supplier influence

- Mitigants: buffer stock and nearshoring raise working capital

- Net: moderate-to-high supplier power

Moderate-high supplier power; 3-12m validation and 60-65% East Asia reliance

Supplier power is moderate–high for Carl Zeiss Meditec: limited optics/sensor vendors and long validation (3–12 months) squeeze margins despite 2024 revenue ~EUR1.9bn. East Asia supplied ~60–65% of advanced components in 2024; image-sensor market ~$22bn. Dual-sourcing and buffers mitigate risk but raise working capital.

| Metric | 2024 |

|---|---|

| Revenue | EUR 1.9bn |

| East Asia share | 60–65% |

| Image-sensor mkt | $22bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Carl Zeiss Meditec, with detailed assessment of threats from substitutes and new entrants. Evaluates supplier and buyer power, identifies disruptive forces, and highlights strategic levers that protect incumbency and drive sustainable profitability.

Clear, one-sheet Porter's Five Forces for Carl Zeiss Meditec—instantly visualize competitive pressure with a radar chart, customize inputs for regulatory shifts or new entrants, and drop the clean layout straight into pitch decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Large hospital systems and GPOs

Large hospital systems and GPOs exert strong buyer power: group purchasing and tenders drive price pressure and standardization, with GPOs accounting for around 70% of US hospital purchasing in 2024, enabling buyers to extract volume discounts and bundled service deals. Multi-year framework agreements shift leverage to sophisticated purchasers, forcing vendors like Carl Zeiss Meditec to compete on total cost of ownership, not just unit price.

Ophthalmology chains and ASCs

High throughput in ophthalmology—about 3.7 million US cataract procedures annually and ~20 million globally in 2024—makes device uptime and per-procedure cost critical for chains and ASCs. Buyers run detailed ROI models comparing platforms, and brand switching at expansion points raises their bargaining power. Service SLAs and financing terms routinely decide deals, often outweighing small tech differentials.

Reimbursement-driven decision making

Reimbursement-driven buying gives customers leverage: capital spend hinges on coding, coverage and tariff levels, so flat reimbursement prompts buyers to demand lower equipment prices or consumable discounts. Carl Zeiss Meditec reported revenue of EUR 1.74bn in FY2024, yet premium pricing depends on demonstrated clinical efficacy; evidence gaps weaken vendor pricing power. In the US Medicare covers about 80% of cataract procedures, amplifying payer influence.

Training and workflow integration

Deep EMR/PACS integration and surgeon training create high switching costs that reduce buyer power; as of 2024 over 96% of US hospitals use certified EHRs (ONC trend), increasing lock‑in for integrated devices, while interoperable offerings expand buyer options and post‑sale support quality materially shifts negotiation leverage.

- Integration lock‑in: high switching costs

- Interoperability: increases buyer options

- Support quality: major negotiation factor

International tender dynamics

Public international tenders for medical devices focus on lowest compliant bid and lifecycle cost, reinforcing price competition; OECD estimates public procurement at about 12% of GDP, underscoring scale and buyer leverage. Transparent, rule-based scoring in many jurisdictions limits differentiation premiums, while local content rules (increasingly used in 2020s) shift bargaining power to regional buyers; overall buyer power is moderate-to-high.

- OECD: public procurement ≈12% of GDP

- Lowest compliant bid + lifecycle costing → price-focused awards

- Transparent scoring reduces differentiation premiums

- Local content rules increase regional buyer leverage

- Buyer power: moderate-to-high

GPO-driven pricing and per-procedure cost dominate high-volume cataract device markets

Large hospital systems and GPOs (≈70% of US hospital purchasing in 2024) drive price pressure; buyers demand TCO, SLAs and bundled deals. High procedure volumes (~3.7M US cataracts, ~20M global in 2024) make per‑procedure cost and uptime decisive. Reimbursement dependence (Medicare ≈80% of US cataracts) increases buyer leverage; integration lock‑in partially offsets power.

| Metric | Value |

|---|---|

| GPO share (US) | ≈70% |

| Cataracts (US/global, 2024) | 3.7M / 20M |

| Meditec revenue FY2024 | EUR 1.74bn |

| Public procurement (OECD) | ≈12% GDP |

Preview the Actual Deliverable

Carl Zeiss Meditec Porter's Five Forces Analysis

This preview shows the exact Carl Zeiss Meditec Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the fully formatted, professional file ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical report.