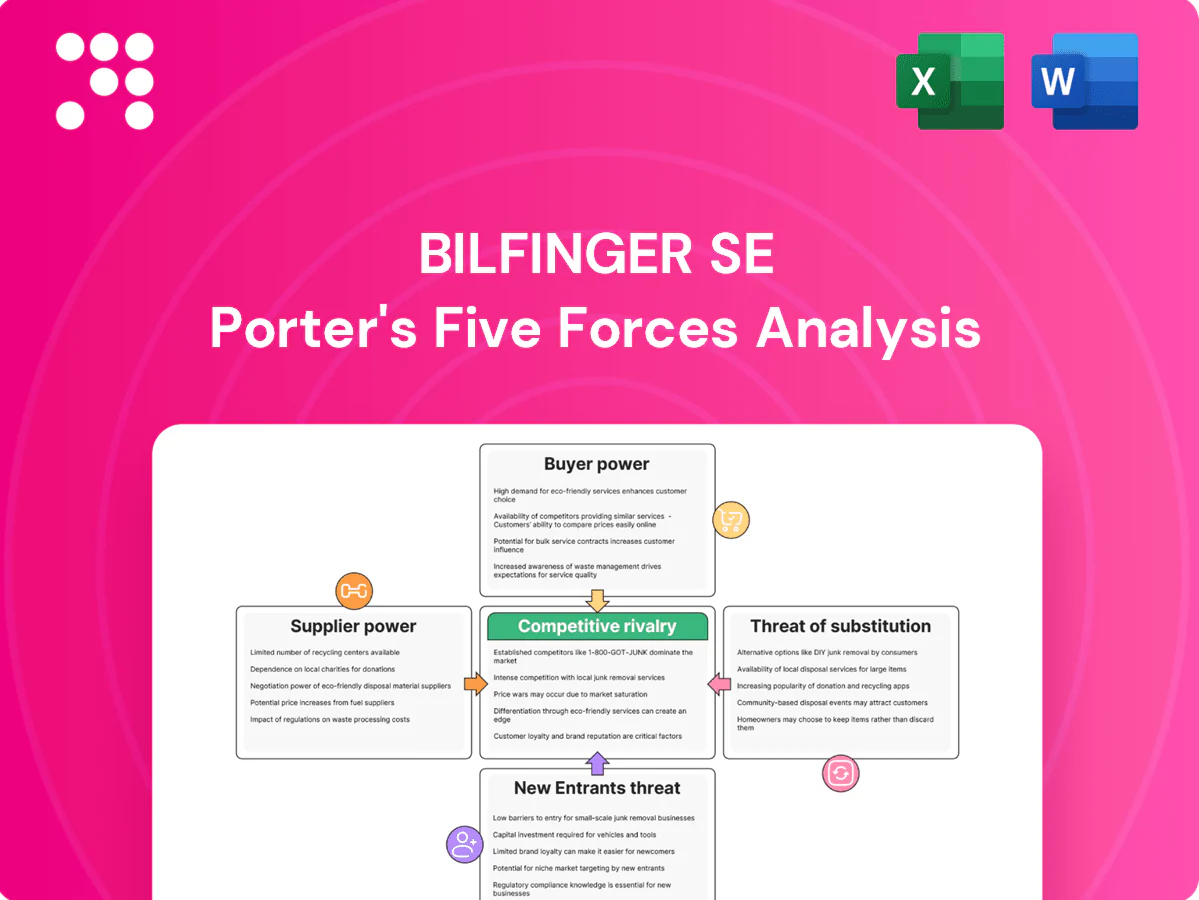

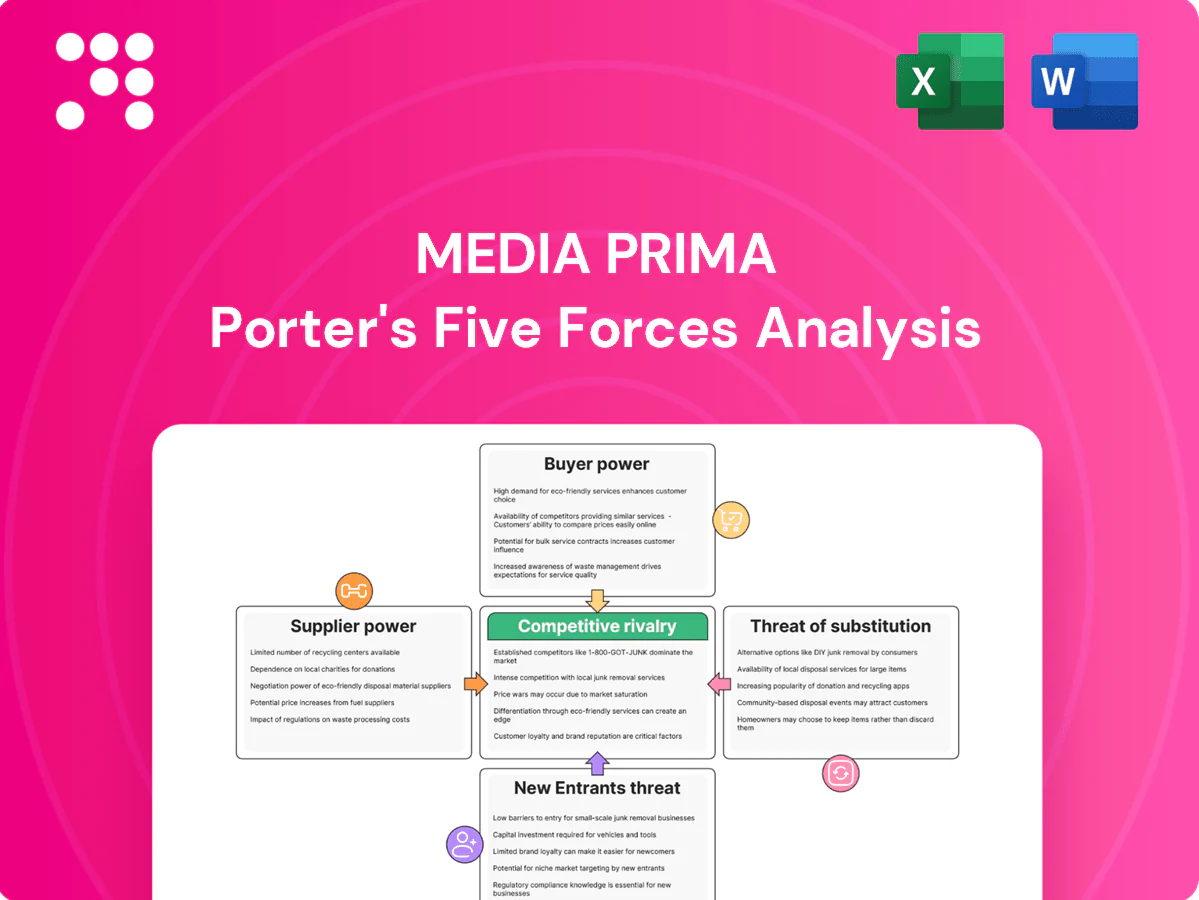

Media Prima Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Media Prima faces moderate competitive rivalry as traditional TV advertising declines while digital streaming grows, with buyer power rising from advertisers and subscribers shifting platforms. Supplier influence is limited but content costs and tech partners matter. Barriers to entry are moderate due to brand and distribution scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Content creators and talent

Star producers, celebrities and independent studios command premium fees and favorable terms, leveraging growing regional OTT demand; their switching threat is credible as alternative platforms and regional streamers expand. Media Prima's Primeworks Studios provides in-house production capacity that partially mitigates supplier leverage through long-term relationships. Talent exclusivity deals and IP ownership remain key negotiation levers in sourcing and cost control.

Technology and distribution vendors

Broadcast equipment, cloud (AWS ~32%, Azure ~23%, GCP ~11% in 2024), CDN and ad-tech providers create high switching costs and integration risk for Media Prima, boosting supplier leverage. Limited local niche suppliers in Malaysia further elevate pricing power. Multi-vendor architectures and open standards mitigate lock-in, while volume commitments and multi-year cloud/CDN contracts typically unlock stronger SLAs (99.9–99.99%) and discounts (often 10–40%).

Telecoms and platform partners

Mobile operators, ISPs and OTT platforms shape reach and data costs for Media Prima: Malaysia recorded 144% mobile penetration per MCMC 2024 while global OTT reach (Netflix 247m subs in Q1 2024) raises distribution leverage. Bundling and zero-rating deals materially affect audience access and ad monetization; dominant telcos with multi‑million subscribers exert pricing leverage. Reciprocal content licensing and co‑marketing partnerships provide countervailing value.

News wires and rights holders

News wires and rights holders control scarce, time-sensitive content, with the global sports and entertainment rights market estimated at roughly USD 50 billion in 2024, keeping supplier leverage high.

Competitive auctions drive price inflation and exclusivity constraints, pressuring margins for broadcasters like Media Prima.

Diversifying into owned newsrooms, local IP, windowing and sublicensing improves content control and can optimize ROI.

- Market size: ~USD 50bn (2024)

- Risk: auction-driven price pressure

- Mitigation: owned IP, windowing, sublicensing

Print and production inputs

Paper, ink and printing services face ongoing global price volatility and episodic supply shocks; top pulp producers account for roughly 40% of global capacity in 2024, increasing supplier leverage while logistics bottlenecks raise lead times. Declining print volumes in Malaysia (double-digit drops year-on-year in newspaper circulation through 2023–24) reduce Media Prima’s scale advantage. Forward contracts and strategic inventory hedging have limited cost swings, cutting raw-material exposure by an estimated 10–15% in 2024.

- Concentration: top producers ~40% of capacity (2024)

- Demand hit: double-digit print circulation declines Y/Y to 2024

- Mitigation: hedging/forwards ~10–15% exposure reduction (2024)

Supplier leverage: cloud lock-in & scarce rights; hedging cuts 10–15%

Suppliers exert high leverage: talent/IP exclusivity, cloud/CDN lock‑in (AWS ~32%, Azure ~23%, GCP ~11% 2024) and scarce sports/entertainment rights (market ~USD 50bn 2024) raise costs. Mobile/ISP distribution (Malaysia mobile penetration 144% MCMC 2024) and concentrated pulp supply (~40% capacity) further strengthen suppliers. Media Prima mitigates via Primeworks, owned IP, windowing, sublicensing and hedging (cost exposure reduction ~10–15% 2024).

| Metric | 2024 Value |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Mobile penetration MY | 144% |

| Rights market | ~USD 50bn |

| Pulp concentration | ~40% |

| Hedging impact | ~10–15% cost reduction |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Media Prima, identifying disruptive forces, substitutes, and emerging threats that challenge market share; evaluates supplier and buyer control and their impact on pricing and profitability to inform strategic positioning.

A clear one-sheet Porter's Five Forces for Media Prima that converts complex competitive pressures into a customizable spider/radar chart—ready to copy into pitch decks or Excel dashboards, swap in your own data, and use without macros.

Customers Bargaining Power

Advertisers and agencies

Large advertisers and holding-company agencies now consolidate over 50% of global media-buying budgets (2024), demanding measurable ROI and centralized rates that squeeze regional sellers like Media Prima. Programmatic buying, which accounts for roughly 70% of global digital display transactions in 2024, and cross-media benchmarking intensify price pressure. Media Prima offsets this by selling integrated solutions and leveraging first-party data to secure premium CPMs. Long-term deals and bundled TV/digital packages reduce advertiser switching.

Audience fragmentation

Viewers can switch across free TV, radio, portals and global OTT at low cost, driven by Malaysia's 2024 internet penetration of 92% (≈30.6M) and 27.6M social media users. High substitutability raises demands for quality and convenience, pushing platforms to match UX and localized content. Superior UX and localized programming reduce churn risk. Multi-platform distribution preserves reach and frequency.

SMEs and digital-native buyers

SMEs and digital-native buyers increasingly compare CPMs/CPCs across walled gardens and local inventory, pressuring Media Prima as global digital ad spend exceeded 600 billion USD in 2024 and buyers shop for relative yield.

Wider rollout of self-serve ad tools and real-time reporting raises transparency and negotiation power, shortening sales cycles and reducing APCs for small buyers.

Simplified products with performance guarantees and 2024 case studies showing higher ROAS attract SME budgets and lift willingness to pay.

Government and GLC advertisers

Public-sector campaigns are material and cyclical, often spiking around election or policy windows, but come with strict compliance and tender conditions that compress margins.

Procurement-driven pricing and payment terms commonly extend to 60–120 days, squeezing cash flow and reducing effective yield from government and GLC advertisers.

Media Prima’s nationwide TV/digital reach and editorial credibility remain differentiators; a balanced client mix limits concentration risk and stabilizes revenue.

- Compliance-driven tenders

- Payment terms: 60–120 days

- Nationwide reach—credibility edge

- Balanced client mix reduces concentration risk

Subscription and pay content users

Where pay products exist, consumers remain highly price sensitive given abundant free news and entertainment alternatives, and Malaysia recorded about 99% internet penetration in 2024 supporting easy access to free substitutes. Churn for Media Prima’s subscription tiers reacts sharply to exclusive content drops and UX issues; industry SVOD churn averages near 3–4% monthly in SEA 2024. Bundles with telcos and tiered pricing improve stickiness, while loyalty programs and community features raise perceived value and ARPU.

- Price sensitivity — abundant free options, 99% internet reach (2024)

- Churn drivers — exclusive drops and UX; SEA SVOD churn ~3–4% monthly (2024)

- Retention levers — telco bundles, tiered pricing

- Value add — loyalty programs, community features boost ARPU

Buyer concentration and programmatic dominance squeeze Malaysian publishers; payment terms bite margins

Major buyers consolidate >50% media budgets (2024) and programmatic buys ~70% of digital display (2024), raising price pressure; Media Prima offsets via integrated, first-party-data packages and long-term bundles. Malaysian internet penetration 92% (≈30.6M) and 27.6M social users increase substitutability. Procurement terms (60–120 days) and public tenders compress margins.

| Metric | 2024 |

|---|---|

| Buyer concentration | >50% |

| Programmatic share | ~70% |

| Malaysia internet | 92% (≈30.6M) |

| Global digital ad spend | >$600B |

| Payment terms | 60–120 days |

Preview Before You Purchase

Media Prima Porter's Five Forces Analysis

This preview shows the exact Media Prima Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use, containing the complete strategic assessment and supporting insights.

Original: $10.00

-70%$10.00

$3.00

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Media Prima faces moderate competitive rivalry as traditional TV advertising declines while digital streaming grows, with buyer power rising from advertisers and subscribers shifting platforms. Supplier influence is limited but content costs and tech partners matter. Barriers to entry are moderate due to brand and distribution scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Content creators and talent

Star producers, celebrities and independent studios command premium fees and favorable terms, leveraging growing regional OTT demand; their switching threat is credible as alternative platforms and regional streamers expand. Media Prima's Primeworks Studios provides in-house production capacity that partially mitigates supplier leverage through long-term relationships. Talent exclusivity deals and IP ownership remain key negotiation levers in sourcing and cost control.

Technology and distribution vendors

Broadcast equipment, cloud (AWS ~32%, Azure ~23%, GCP ~11% in 2024), CDN and ad-tech providers create high switching costs and integration risk for Media Prima, boosting supplier leverage. Limited local niche suppliers in Malaysia further elevate pricing power. Multi-vendor architectures and open standards mitigate lock-in, while volume commitments and multi-year cloud/CDN contracts typically unlock stronger SLAs (99.9–99.99%) and discounts (often 10–40%).

Telecoms and platform partners

Mobile operators, ISPs and OTT platforms shape reach and data costs for Media Prima: Malaysia recorded 144% mobile penetration per MCMC 2024 while global OTT reach (Netflix 247m subs in Q1 2024) raises distribution leverage. Bundling and zero-rating deals materially affect audience access and ad monetization; dominant telcos with multi‑million subscribers exert pricing leverage. Reciprocal content licensing and co‑marketing partnerships provide countervailing value.

News wires and rights holders

News wires and rights holders control scarce, time-sensitive content, with the global sports and entertainment rights market estimated at roughly USD 50 billion in 2024, keeping supplier leverage high.

Competitive auctions drive price inflation and exclusivity constraints, pressuring margins for broadcasters like Media Prima.

Diversifying into owned newsrooms, local IP, windowing and sublicensing improves content control and can optimize ROI.

- Market size: ~USD 50bn (2024)

- Risk: auction-driven price pressure

- Mitigation: owned IP, windowing, sublicensing

Print and production inputs

Paper, ink and printing services face ongoing global price volatility and episodic supply shocks; top pulp producers account for roughly 40% of global capacity in 2024, increasing supplier leverage while logistics bottlenecks raise lead times. Declining print volumes in Malaysia (double-digit drops year-on-year in newspaper circulation through 2023–24) reduce Media Prima’s scale advantage. Forward contracts and strategic inventory hedging have limited cost swings, cutting raw-material exposure by an estimated 10–15% in 2024.

- Concentration: top producers ~40% of capacity (2024)

- Demand hit: double-digit print circulation declines Y/Y to 2024

- Mitigation: hedging/forwards ~10–15% exposure reduction (2024)

Supplier leverage: cloud lock-in & scarce rights; hedging cuts 10–15%

Suppliers exert high leverage: talent/IP exclusivity, cloud/CDN lock‑in (AWS ~32%, Azure ~23%, GCP ~11% 2024) and scarce sports/entertainment rights (market ~USD 50bn 2024) raise costs. Mobile/ISP distribution (Malaysia mobile penetration 144% MCMC 2024) and concentrated pulp supply (~40% capacity) further strengthen suppliers. Media Prima mitigates via Primeworks, owned IP, windowing, sublicensing and hedging (cost exposure reduction ~10–15% 2024).

| Metric | 2024 Value |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Mobile penetration MY | 144% |

| Rights market | ~USD 50bn |

| Pulp concentration | ~40% |

| Hedging impact | ~10–15% cost reduction |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Media Prima, identifying disruptive forces, substitutes, and emerging threats that challenge market share; evaluates supplier and buyer control and their impact on pricing and profitability to inform strategic positioning.

A clear one-sheet Porter's Five Forces for Media Prima that converts complex competitive pressures into a customizable spider/radar chart—ready to copy into pitch decks or Excel dashboards, swap in your own data, and use without macros.

Customers Bargaining Power

Advertisers and agencies

Large advertisers and holding-company agencies now consolidate over 50% of global media-buying budgets (2024), demanding measurable ROI and centralized rates that squeeze regional sellers like Media Prima. Programmatic buying, which accounts for roughly 70% of global digital display transactions in 2024, and cross-media benchmarking intensify price pressure. Media Prima offsets this by selling integrated solutions and leveraging first-party data to secure premium CPMs. Long-term deals and bundled TV/digital packages reduce advertiser switching.

Audience fragmentation

Viewers can switch across free TV, radio, portals and global OTT at low cost, driven by Malaysia's 2024 internet penetration of 92% (≈30.6M) and 27.6M social media users. High substitutability raises demands for quality and convenience, pushing platforms to match UX and localized content. Superior UX and localized programming reduce churn risk. Multi-platform distribution preserves reach and frequency.

SMEs and digital-native buyers

SMEs and digital-native buyers increasingly compare CPMs/CPCs across walled gardens and local inventory, pressuring Media Prima as global digital ad spend exceeded 600 billion USD in 2024 and buyers shop for relative yield.

Wider rollout of self-serve ad tools and real-time reporting raises transparency and negotiation power, shortening sales cycles and reducing APCs for small buyers.

Simplified products with performance guarantees and 2024 case studies showing higher ROAS attract SME budgets and lift willingness to pay.

Government and GLC advertisers

Public-sector campaigns are material and cyclical, often spiking around election or policy windows, but come with strict compliance and tender conditions that compress margins.

Procurement-driven pricing and payment terms commonly extend to 60–120 days, squeezing cash flow and reducing effective yield from government and GLC advertisers.

Media Prima’s nationwide TV/digital reach and editorial credibility remain differentiators; a balanced client mix limits concentration risk and stabilizes revenue.

- Compliance-driven tenders

- Payment terms: 60–120 days

- Nationwide reach—credibility edge

- Balanced client mix reduces concentration risk

Subscription and pay content users

Where pay products exist, consumers remain highly price sensitive given abundant free news and entertainment alternatives, and Malaysia recorded about 99% internet penetration in 2024 supporting easy access to free substitutes. Churn for Media Prima’s subscription tiers reacts sharply to exclusive content drops and UX issues; industry SVOD churn averages near 3–4% monthly in SEA 2024. Bundles with telcos and tiered pricing improve stickiness, while loyalty programs and community features raise perceived value and ARPU.

- Price sensitivity — abundant free options, 99% internet reach (2024)

- Churn drivers — exclusive drops and UX; SEA SVOD churn ~3–4% monthly (2024)

- Retention levers — telco bundles, tiered pricing

- Value add — loyalty programs, community features boost ARPU

Buyer concentration and programmatic dominance squeeze Malaysian publishers; payment terms bite margins

Major buyers consolidate >50% media budgets (2024) and programmatic buys ~70% of digital display (2024), raising price pressure; Media Prima offsets via integrated, first-party-data packages and long-term bundles. Malaysian internet penetration 92% (≈30.6M) and 27.6M social users increase substitutability. Procurement terms (60–120 days) and public tenders compress margins.

| Metric | 2024 |

|---|---|

| Buyer concentration | >50% |

| Programmatic share | ~70% |

| Malaysia internet | 92% (≈30.6M) |

| Global digital ad spend | >$600B |

| Payment terms | 60–120 days |

Preview Before You Purchase

Media Prima Porter's Five Forces Analysis

This preview shows the exact Media Prima Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use, containing the complete strategic assessment and supporting insights.