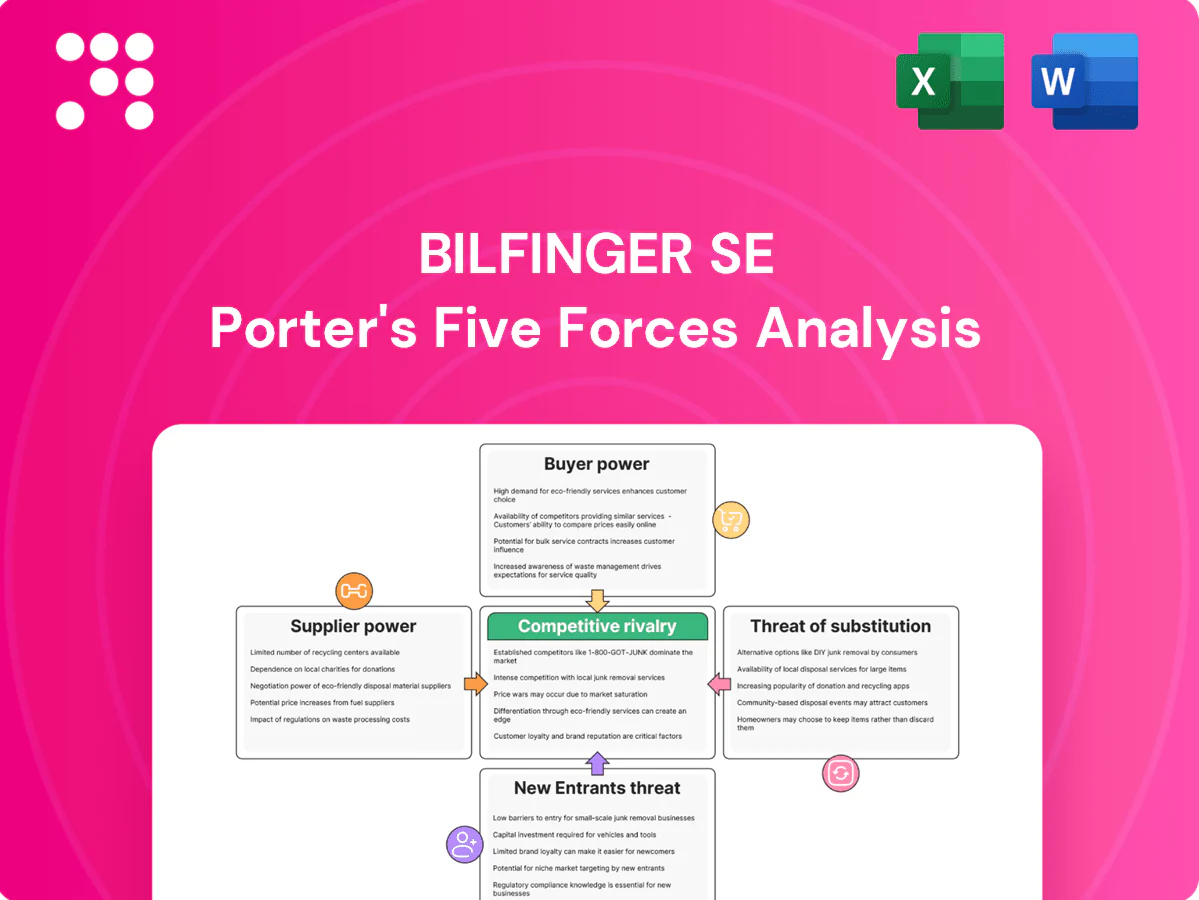

Foot Locker Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Foot Locker faces fierce rivalry from athletic brands and online retailers, while buyer power rises with price transparency and omnichannel options. Supplier leverage is moderate given brand relationships, but new digital entrants and substitutes pressure margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Foot Locker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated brand vendors

Foot Locker depends heavily on a handful of global brands—Nike (including Jordan), Adidas and New Balance—with Nike/Jordan estimated to drive roughly 50% of branded merchandise sales in 2023, concentrating revenue exposure. This vendor concentration boosts supplier leverage over pricing, allocations and promotional terms, constraining Foot Locker’s margin flexibility. Any loss or reduced allocation from a top brand can materially cut traffic and sales mix, elevating supplier bargaining power despite Foot Locker’s scale.

Direct-to-consumer shift

Leading brands prioritize DTC and data, restricting wholesale allocations, shortening product life cycles and tightening margins; Nike's DTC approached 40% of sales while Foot Locker reported roughly $6.9B in net sales in 2023. Foot Locker must deliver incremental distribution, storytelling and in-store experiences to remain vital. The DTC tilt structurally strengthens supplier bargaining power over wholesale partners.

Exclusive drops and allocations

High-heat launches and exclusives are controlled by brands, with StockX reporting in 2024 that top sneaker drops often command resale premiums exceeding 200%, underscoring brand pricing power.

Allocation decisions reward partners that deliver superior omnichannel execution and community reach, giving brands leverage to favor select retailers.

Dependence on launch calendars gives vendors negotiation power; Foot Locker’s ability to secure some exclusives mitigates but does not erase supplier power.

Terms, MAP, and compliance

Suppliers dictate wholesale pricing, MAP policies, shop-in-shop standards and visual merchandising, limiting Foot Locker’s ability to set price and in-store presentation; non-compliance can lead vendors to reduce allocations or delist accounts.

- Vendor control: enforces MAP and visual standards

- Risk: non-compliance jeopardizes allocations

- Impact: compresses retailer pricing flexibility

- Leverage: brand equity lets vendors set strict terms

Diversification and private label limits

Foot Locker is broadening its brand mix and developing owned brands while reporting roughly $6.0 billion in net sales in fiscal 2024; however demand remains skewed to marquee labels. Private-label penetration stayed under 10% in 2024, constraining substitution away from powerful suppliers. Vendor diversification only partially offsets supplier power as top suppliers (Nike, Adidas) still represent about 65% of purchases.

- Owned brands expanding but low share

- Private label <10% of sales (2024)

- Top vendors ~65% purchase concentration (2024)

50% brand, 65% vendor risk, DTC 40%

Foot Locker relies on Nike/Jordan (~50% of branded merchandise sales in 2023) and top vendors (~65% of purchases in 2024), concentrating supplier power. Brands' DTC share near 40% and tight allocations/exclusive drops (resale premiums >200% in 2024) limit Foot Locker pricing and SKU control. Private label <10% (2024) and $6.0B net sales (FY2024) mean diversification only partially offsets supplier leverage.

| Metric | Value | Year |

|---|---|---|

| Nike/Jordan share | ~50% | 2023 |

| Top vendors purchase concentration | ~65% | 2024 |

| Nike DTC | ~40% | 2023 |

| Private label | <10% | 2024 |

| Net sales | $6.0B | FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis of Foot Locker uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and margins.

One-sheet Porter's Five Forces for Foot Locker that distills competitive pressures into a customizable radar chart—perfect for rapid decision-making and slide-ready summaries; swap in current data or scenario tabs to model new entrants, supplier shifts, or retail trends without macros.

Customers Bargaining Power

High price transparency

High price transparency lets consumers compare prices instantly across DTC sites and rivals, and with global e-commerce at about 23% of retail sales in 2024 buyers can shop broadly in seconds. Low switching costs force retailers into promotions and price-matching, eroding margins and raising buyer leverage. Digital-savvy shoppers increasingly expect the best price plus fast delivery, intensifying pressure on Foot Locker's pricing strategies.

Hype versus elasticity

For limited releases buyers exhibit low price sensitivity and high urgency, often paying premiums on secondary markets that elevate Foot Locker’s bargaining leverage for those SKUs.

By contrast, general inline product shows high promotion sensitivity, with sell-through and margin outcomes hinging on markdown cadence and promotional depth.

Careful assortment planning and strict markdown discipline are required, as the mix between hyped drops and core inventory determines realized buyer power at any time.

Omnichannel expectations

Shoppers expect seamless BOPIS, fast shipping, easy returns, and inventory visibility; failure on convenience drives immediate switching, increasing customer bargaining power. Strong omnichannel execution—tight inventory sync, reliable fulfillment, and unified customer data—reduces buyer power by adding utility and friction to switching. Loyalty programs, a smooth app UX, and personalized offers further lock in spend and lower price sensitivity.

Loyalty and community effects

FLX and similar programs lock in repeat purchases by offering points, early access to drops and members-only perks, reducing immediate price sensitivity; Foot Locker reported FLX surpassed 2 million members by 2024, helping boost repeat engagement.

Community events, creator content and exclusive drops create non-price differentiation, but benefits must clearly exceed competitors like Nike and Adidas CONFIRMED loyalty offers to truly constrain buyer power.

- FLX members >2M (2024)

- Early access lowers price elasticity

- Events/content = non-price switching costs

- Must outvalue rival programs to limit buyer power

Wide alternative access

Wide alternative access empowers customers: they can buy brand DTC, competitors such as JD Sports, Finish Line, Dick’s, Hibbett, or via marketplaces like Amazon and StockX, making cross-shopping habitual in sneakers and raising buyers’ negotiating power. Foot Locker must win on in‑store experience, curated assortments, and trust to offset switching.

- Omnichannel choices increase buyer leverage

- Cross‑shopping common among sneaker buyers

- Experience, curation, trust are differentiators

E‑commerce transparency and low switching costs squeeze margins; loyalty sustains selective pricing

High price transparency and low switching costs (global e‑commerce ~23% of retail sales in 2024) force promotions and margin pressure; limited drops, however, give Foot Locker pricing power on select SKUs. FLX loyalty (over 2 million members in 2024) reduces short‑term price sensitivity, while omnichannel choice and marketplaces keep overall buyer leverage elevated.

| Metric | 2024 |

|---|---|

| Global e‑commerce share | ~23% |

| FLX members | >2,000,000 |

Preview Before You Purchase

Foot Locker Porter's Five Forces Analysis

This preview shows the exact Foot Locker Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no abridgments. The full document is professionally written, fully formatted and ready for immediate download and use. You’re viewing the deliverable itself, so once you buy you get instant access to this same complete file.

Original: $10.00

-70%$10.00

$3.00

Description

Don't Miss the Bigger Picture

Foot Locker faces fierce rivalry from athletic brands and online retailers, while buyer power rises with price transparency and omnichannel options. Supplier leverage is moderate given brand relationships, but new digital entrants and substitutes pressure margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Foot Locker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated brand vendors

Foot Locker depends heavily on a handful of global brands—Nike (including Jordan), Adidas and New Balance—with Nike/Jordan estimated to drive roughly 50% of branded merchandise sales in 2023, concentrating revenue exposure. This vendor concentration boosts supplier leverage over pricing, allocations and promotional terms, constraining Foot Locker’s margin flexibility. Any loss or reduced allocation from a top brand can materially cut traffic and sales mix, elevating supplier bargaining power despite Foot Locker’s scale.

Direct-to-consumer shift

Leading brands prioritize DTC and data, restricting wholesale allocations, shortening product life cycles and tightening margins; Nike's DTC approached 40% of sales while Foot Locker reported roughly $6.9B in net sales in 2023. Foot Locker must deliver incremental distribution, storytelling and in-store experiences to remain vital. The DTC tilt structurally strengthens supplier bargaining power over wholesale partners.

Exclusive drops and allocations

High-heat launches and exclusives are controlled by brands, with StockX reporting in 2024 that top sneaker drops often command resale premiums exceeding 200%, underscoring brand pricing power.

Allocation decisions reward partners that deliver superior omnichannel execution and community reach, giving brands leverage to favor select retailers.

Dependence on launch calendars gives vendors negotiation power; Foot Locker’s ability to secure some exclusives mitigates but does not erase supplier power.

Terms, MAP, and compliance

Suppliers dictate wholesale pricing, MAP policies, shop-in-shop standards and visual merchandising, limiting Foot Locker’s ability to set price and in-store presentation; non-compliance can lead vendors to reduce allocations or delist accounts.

- Vendor control: enforces MAP and visual standards

- Risk: non-compliance jeopardizes allocations

- Impact: compresses retailer pricing flexibility

- Leverage: brand equity lets vendors set strict terms

Diversification and private label limits

Foot Locker is broadening its brand mix and developing owned brands while reporting roughly $6.0 billion in net sales in fiscal 2024; however demand remains skewed to marquee labels. Private-label penetration stayed under 10% in 2024, constraining substitution away from powerful suppliers. Vendor diversification only partially offsets supplier power as top suppliers (Nike, Adidas) still represent about 65% of purchases.

- Owned brands expanding but low share

- Private label <10% of sales (2024)

- Top vendors ~65% purchase concentration (2024)

50% brand, 65% vendor risk, DTC 40%

Foot Locker relies on Nike/Jordan (~50% of branded merchandise sales in 2023) and top vendors (~65% of purchases in 2024), concentrating supplier power. Brands' DTC share near 40% and tight allocations/exclusive drops (resale premiums >200% in 2024) limit Foot Locker pricing and SKU control. Private label <10% (2024) and $6.0B net sales (FY2024) mean diversification only partially offsets supplier leverage.

| Metric | Value | Year |

|---|---|---|

| Nike/Jordan share | ~50% | 2023 |

| Top vendors purchase concentration | ~65% | 2024 |

| Nike DTC | ~40% | 2023 |

| Private label | <10% | 2024 |

| Net sales | $6.0B | FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis of Foot Locker uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and margins.

One-sheet Porter's Five Forces for Foot Locker that distills competitive pressures into a customizable radar chart—perfect for rapid decision-making and slide-ready summaries; swap in current data or scenario tabs to model new entrants, supplier shifts, or retail trends without macros.

Customers Bargaining Power

High price transparency

High price transparency lets consumers compare prices instantly across DTC sites and rivals, and with global e-commerce at about 23% of retail sales in 2024 buyers can shop broadly in seconds. Low switching costs force retailers into promotions and price-matching, eroding margins and raising buyer leverage. Digital-savvy shoppers increasingly expect the best price plus fast delivery, intensifying pressure on Foot Locker's pricing strategies.

Hype versus elasticity

For limited releases buyers exhibit low price sensitivity and high urgency, often paying premiums on secondary markets that elevate Foot Locker’s bargaining leverage for those SKUs.

By contrast, general inline product shows high promotion sensitivity, with sell-through and margin outcomes hinging on markdown cadence and promotional depth.

Careful assortment planning and strict markdown discipline are required, as the mix between hyped drops and core inventory determines realized buyer power at any time.

Omnichannel expectations

Shoppers expect seamless BOPIS, fast shipping, easy returns, and inventory visibility; failure on convenience drives immediate switching, increasing customer bargaining power. Strong omnichannel execution—tight inventory sync, reliable fulfillment, and unified customer data—reduces buyer power by adding utility and friction to switching. Loyalty programs, a smooth app UX, and personalized offers further lock in spend and lower price sensitivity.

Loyalty and community effects

FLX and similar programs lock in repeat purchases by offering points, early access to drops and members-only perks, reducing immediate price sensitivity; Foot Locker reported FLX surpassed 2 million members by 2024, helping boost repeat engagement.

Community events, creator content and exclusive drops create non-price differentiation, but benefits must clearly exceed competitors like Nike and Adidas CONFIRMED loyalty offers to truly constrain buyer power.

- FLX members >2M (2024)

- Early access lowers price elasticity

- Events/content = non-price switching costs

- Must outvalue rival programs to limit buyer power

Wide alternative access

Wide alternative access empowers customers: they can buy brand DTC, competitors such as JD Sports, Finish Line, Dick’s, Hibbett, or via marketplaces like Amazon and StockX, making cross-shopping habitual in sneakers and raising buyers’ negotiating power. Foot Locker must win on in‑store experience, curated assortments, and trust to offset switching.

- Omnichannel choices increase buyer leverage

- Cross‑shopping common among sneaker buyers

- Experience, curation, trust are differentiators

E‑commerce transparency and low switching costs squeeze margins; loyalty sustains selective pricing

High price transparency and low switching costs (global e‑commerce ~23% of retail sales in 2024) force promotions and margin pressure; limited drops, however, give Foot Locker pricing power on select SKUs. FLX loyalty (over 2 million members in 2024) reduces short‑term price sensitivity, while omnichannel choice and marketplaces keep overall buyer leverage elevated.

| Metric | 2024 |

|---|---|

| Global e‑commerce share | ~23% |

| FLX members | >2,000,000 |

Preview Before You Purchase

Foot Locker Porter's Five Forces Analysis

This preview shows the exact Foot Locker Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no abridgments. The full document is professionally written, fully formatted and ready for immediate download and use. You’re viewing the deliverable itself, so once you buy you get instant access to this same complete file.